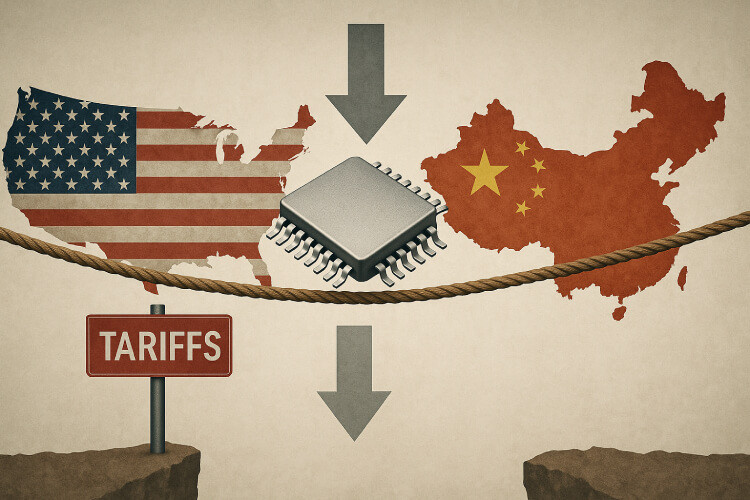

Trump Semiconductor Tariffs 2025: What the 10% Duty Means

Insights | 03-06-2025 | By Robin Mitchell

Key Takeaways:

- The new 2025 semiconductor tariff reprises Trump’s earlier protectionist playbook—this time targeting even close U.S. allies and risking global tech supply chain disruption.

- Electronics rely on deeply globalised manufacturing networks—tariffs threaten to break these chains, inflating costs across industries from automotive to aerospace.

- Rather than countering China, the tariff risks undermining U.S. competitiveness—American firms may end up paying more, rerouting production, or shifting focus to more stable trade environments.

- Mid-2025 will be pivotal—with decisions on full tariff reinstatement or strategic carveouts expected, the industry braces for a potential reshaping of global electronics trade.

Trade policy has always walked a tightrope between economic strategy and political theatre. When wielded with care, tariffs can protect industries, encourage domestic growth, and level competitive playing fields. But when deployed indiscriminately, they risk doing more harm than good, especially in sectors as globally interwoven as electronics. In 2025, the United States finds itself revisiting an old script with a new semiconductor tariff that may end up stifling the very innovation it seeks to foster.

What lessons from Trump’s first-term tariffs are being ignored, how might this new round affect the global tech ecosystem, and could America’s silicon self-sabotage mark the beginning of a strategic retreat from tech leadership?

Trump’s Tariff – A Seriously Misguided Economic Act

By any rational metric, Donald Trump’s tariff playbook is still a textbook example of “good idea, terrible execution.” Protectionism isn’t inherently evil—it has its place. But threatening a blanket tariff on friend and foe alike? That’s not a strategy. That’s a blunt‑force instrument where a scalpel is needed.

Most people, even outside the political or economic sphere, remember the buzz around Trump’s sweeping tariffs during his first term. What many don’t realise is that the new 2025 semiconductor tariff follows the same script: even close allies such as the UK, which actually run a trade deficit with the U.S., would feel the sting.

The stated goal is to bolster domestic manufacturing. Great in theory. The U.S. wants to make more things at home, build stronger internal supply chains, and reduce dependency on foreign production. But theory and practice don’t always shake hands. In electronics, they’re still barely on speaking terms.

Modern electronics don’t get built in one country. That phone in your pocket? Its processor might be designed in California, fabbed in Taiwan, with memory from South Korea, capacitors from Japan, and assembly in Vietnam. Break any link in that chain, and good luck with shipping a finished product.

COVID taught us this the hard way. Factories shut down, ports clogged, and suddenly, everything from automotive ECUs to basic microcontrollers became unicorns. We’re still feeling the aftershocks. The last thing anyone needed was another artificial wrench in the gears—yet that’s exactly what round two of Trump‑era tariffs threatens.

Here’s the kicker: electronics aren’t just an industry—they’re in every industry. Medical, automotive, aerospace, agriculture—you name it, it runs on electronics. Hike the cost of a sensor by even 10 % (the interim duty now in force) and then multiply that across millions of units, hundreds of applications, and every corner of modern life.

Trump’s Semiconductor Tariff – Punching Ourselves in the Silicon

President Trump proposed a 25 % blanket tariff on imported semiconductors in April—but quickly paused the rate and replaced it with a 10 % interim duty while the Commerce Department conducts a Section 232 national‑security probe. The legacy 25 % China‑specific tariff (rising to 50 % once the pause ends) remains in place. In other words, there is no single number you can slap on an invoice today; it depends on where the die was fabbed, and which press release came out this week.

Semiconductors aren’t just another product line; they’re the foundation of everything from smartphones to fighter jets. The soundbite is “level the playing field.” American chip companies do face serious challenges against heavily subsidised Chinese rivals. But here’s the uncomfortable truth: we’re not just sparring with China. We’re also kneecapping our own supply chain (and everyone else’s).

U.S. companies don’t merely design chips—they manufacture, test, package, and assemble them across a globe‑spanning network. Even Intel and AMD rely on fabs in Asia and Europe. The steppers? Dutch. The wafers? Often Japanese. The packaging? Usually Southeast Asian.

China, meanwhile, is pouring billions into semiconductor independence. Tariffs aren’t innovation. Tariffs are a tax paid by American firms, American workers, and American consumers, while China keeps building fabs and stockpiling materials.

It’s not just chip companies taking the hit. Automakers, aerospace contractors, telecom providers, defence suppliers—pretty much anyone who uses silicon—feel the pain. Carmakers still bruised by COVID shortages now face uncertain duties that can add $350–$600 in silicon costs to a mid‑size SUV.

What Happens Next – Tariffs, Trade Deals, and Strategic Backdoors

So, what’s next in this spiralling saga of semiconductor self‑sabotage?

Mid‑July 2025 is the first waypoint: Commerce delivers its Section 232 report. Options range from reinstating the full 25 % blanket duty to locking in the 10 % interim rate or carving out exclusions for allies. History says Trump digs in rather than climbs down.

More likely? He uses tariffs as leverage, pressuring allies into side deals. Countries like the UK, France, and Germany—heavily dependent on stable U.S. demand—might swallow concessions to avoid prolonged disruption. China? Not a chance. Beijing will fight every inch, and that’s risky: China still holds roughly $730 billion in U.S. Treasuries. Dumping even a slice of that pile could rattle bond markets and spike interest rates.

Meanwhile, the electronics industry will do what it always does—adapt, reroute, and exploit loopholes. Expect more components to be funnelled through tariff‑friendly nations with light assembly added just to tick the “country‑of‑origin” box. Voilà: a Chinese‑made PCB becomes a “UK‑manufactured” product, legally fit for U.S. import at the lower interim rate.

Some firms will quietly pivot away from the U.S. Why wrestle with policy whiplash when the EU, Southeast Asia, or Africa offer clearer rules? America risks pricing itself out of the global innovation club.

Worst‑case? Self‑inflicted isolation. As partners seek more predictable tech alliances, U.S. dominance could erode. It won’t happen overnight, but economic ostracism is death by a thousand self‑inflicted cuts. We’re already seeing the tell‑tales: companies hedging bets, governments courting new blocs, and engineers warning of higher prices and slower innovation. The electronics sector, agile yet overburdened, maybe the first to pivot away from U.S. interests—but it won’t be the last.

Bottom line? Tariffs win headlines; they lose markets. In a world built on silicon and code, surrendering ground in semiconductors means surrendering the future.